Introduction

Statkraft Perú S.A. is a power generation company that trades energy and power with free and regulated clients. It is also involved in the short-term market operated by COES – SINAC, where generation companies bridge the gaps between the injections from plant production and the withdrawals to meet contractual commitments at short-term marginal costs. Additionally, the company earns revenues for transmission services from the secondary transmission networks it owns.

In 2014, the total volume of energy sold by Statkraft Perú S.A. (both to clients and to the spot market) amounted to 1,806.4 GWh. This volume of energy sold was 17.2% lower than that recorded in 2013 (2,183.6 GWh).

Even though in 2014 there was an increased consumption from the Milpo Group due to the contract of El Porvenir Unit (15 MW) for contracted capacity, the sales by Statkraft Perú decreased by 17.2% compared to the previous year, due to i) the expiration of one of the contracts entered into with Edelnor (decreased from 530.9 GWh in 2013 to 89.7 GWh in 2014), and ii) the diminished consumption of Doe Run Perú due to the partial suspension of its operations at La Oroya Unit (201.8 GWh less compared to 2013).

As a consequence, in 2014 the energy purchases to Kallpa were also reduced, which were aimed at covering the supply contract with Doe Run Perú – La Oroya Unit. No net purchases in the spot market were made.

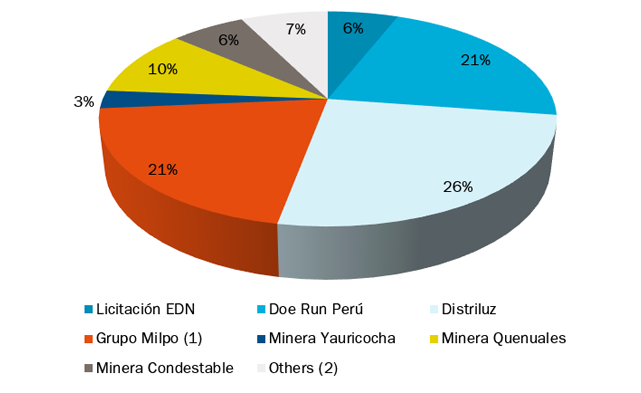

Similarly, it can be observed that 35% of the invoicing of energy and capacity through supply contracts are to power distribution companies, whereas 65% corresponds to free clients.

Chart 3 shows in detail the company’s invoicing of energy and capacity through contracts in 2014, broken down per clients.

Chart 3

The revenues from the secondary transmission system (SST) tolls went down by 4.9% due to a lower demand than the forecast. This difference will be recovered next year during the annual SST revenues settlement process.

The revenues for energy and capacity transfers in COES – SINAC went up by 55.5% compared to 2013 due to a reduction of withdrawals from the spot market as a result of lower sales through supply contracts.

Clients

Statkraft Perú S.A. deems the trading and customer service to be of paramount importance to set apart the service it provides and to maximize the company’s contribution margin.

As a result, the company has close relations and is in constant coordination with clients through electronic mails, phone and letters. The most relevant aspect regarding the interrelation with clients is the coordination of operational issues such as the maintenance of transmission systems, and the coordination of invoicing and accounting issues, including the timely submission of invoices and bank deposits in the company’s accounts.

In 2014, the company had 20 clients in all, as shown in Table 9 according to the type of clients: free clients and distribution companies.

Table 9

Type |

Contract |

Period |

Free Clients |

DOE RUN PERU S.R.L. - La Oroya Unit |

01/01/2009 - 31/12/2015 |

DOE RUN PERU S.R.L. - Cobriza Unit |

01/07/2009 - 31/12/2016 |

|

MINERA CHINALCO PERÚ S.A. |

15/09/2005 - 31/12/2016 |

|

AZULCOCHA MINING S.A. |

01/01/2011 -30/11/2014 |

|

COMPAÑÍA MINERA MILPO S.A.A. - Cerro Lindo Unit |

01/09/2010 - 31/05/2016 |

|

COMPAÑÍA MINERA MILPO S.A.A. - Atacocha Unit |

01/02/2012 - 31/05/2016 |

|

COMPAÑÍA MINERA MILPO S.A.A. - El Porvenir Unit |

01/02/2014 - 31/05/2016 |

|

TREVALI PERU S.A.C. |

01/02/2013 - 31/12/2016 |

|

EMPRESA MINERA LOS QUENUALES S.A. |

01/01/2013 - 31/12/2017 |

|

COMPAÑÍA MINERA CONDESTABLE S.A. |

09/02/2014 - 28/02/2019 |

|

SOCIEDAD MINERA CORONA S.A. |

01/11/2013 - 31/10/2023 |

|

BANCO CONTINENTAL |

01/12/2014 - 31/12/2019 |

|

Distribution Companies |

ADINELSA |

01/10/2011 - 31/12/2014 |

COELVISAC |

01/01/2013 - 31/12/2022 |

|

ELECTROCENTRO |

01/01/2013 - 31/12/2022 |

|

ENOSA |

01/01/2013 - 31/12/2022 |

|

ENSA |

01/01/2013 - 31/12/2022 |

|

HIDRANDINA |

01/01/2013 - 31/12/2022 |

|

EDELNOR |

01/01/2014 - 31/10/2014 |

|

LUZ DEL SUR S.A.A. |

01/01/2014 - 31/10/2014 |

|

SEAL |

01/01/2014 - 31/10/2014 |

|

ESEMPAT |

01/09/2009 - 30/09/2015 |

|

COCHAS DISTRICT MUNICIPALITY |

01/02/2009 -31/12/2015 |

Free clients enter into contracts under a free price regime, whereas distribution companies –electricity utility suppliers- enter into supply contracts through: i) long-term auction processes, or ii) bilateral contracts, in which case the prices regulated by OSINERGMIN apply.

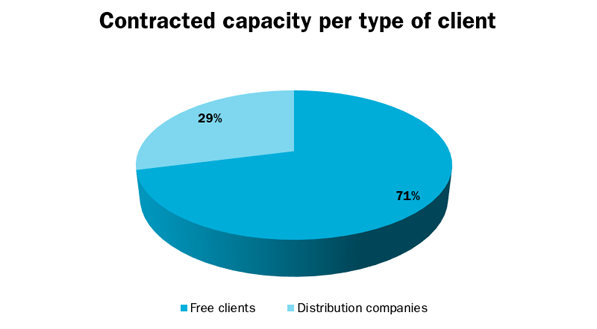

In 2014, the contracted capacity with distribution companies totaled 28.7%, compared to 71.3% of free clients, as shown in Chart 4.

Chart 4

Commercial strategy

The electrical market is experiencing low marginal costs for consecutive years. This is explained by the oversupply of existing generation, the auctions called by the government to increase production with hydropower and non-conventional renewable energy, and the low demand growth. Moreover, as described in section 2.2.1, the spot market has been intervened with Emergency Decree No.049-2008 and Law No.30115.

In this sense, the commercial strategy of Statkraft Perú S.A. takes into consideration the aforementioned context and encompasses the risk assessment guidelines, which are put forward to the company’s Board, as well as the monthly marginal cost forecasts in order to detect contract opportunities to add value to the contribution margin.

As a consequence, the commercial strategy of Statkraft Perú S.A. takes into consideration the total sales of maximum energy authorized in the commercial mandates, according to which the company is authorized to sell energy through bilateral contracts or auction processes. In 2014, Statkraft Perú S.A. entered into a new supply contract with the Banco Continental for 3.3 MW, effective from December 2014 to December 2019 (5-year period). Additionally, an addendum was entered into with Minera Chinalco Perú S.A. to extend the validity of the contract for another 2 years, with a contracted demand of 0.8 MW. This contract becomes effective in January 2015.

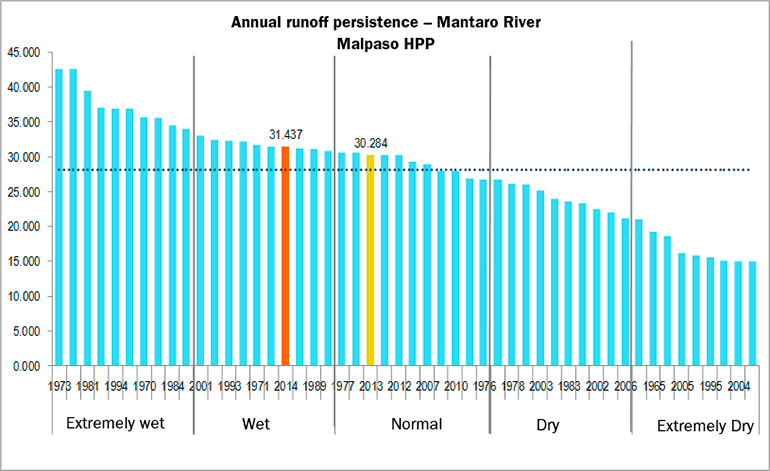

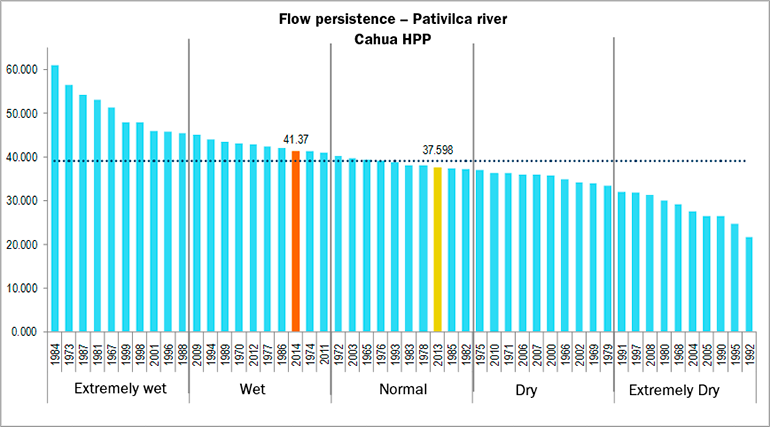

Hydrological information

As part of the commercial strategy, the company constantly monitors the hydrological behavior of the basins where it operates. In 2014, the results, according to the hydrological classification, were as follows:

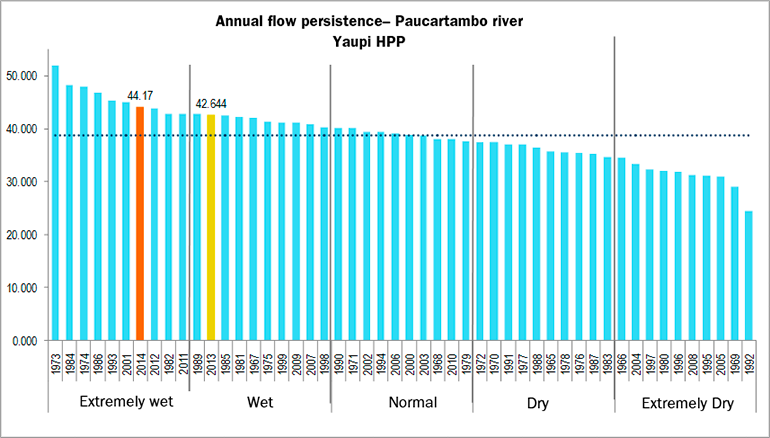

- Paucartambo (Yaupi hydropower plant): extremely wet, with a flow of 44.17 m3/s, greater than that in 2013 (42.64 m3/s).

- Mantaro Alto (Malpaso hydropower plant): wet, with a flow of 31.44 m3/s, slightly greater than that in 2013 (30.28 m3/s).

- Pativilca (Cahua hydropower plant): wet, with a flow of 41.37 m3/s, greater than that in 2013 (37.60 m3/s).

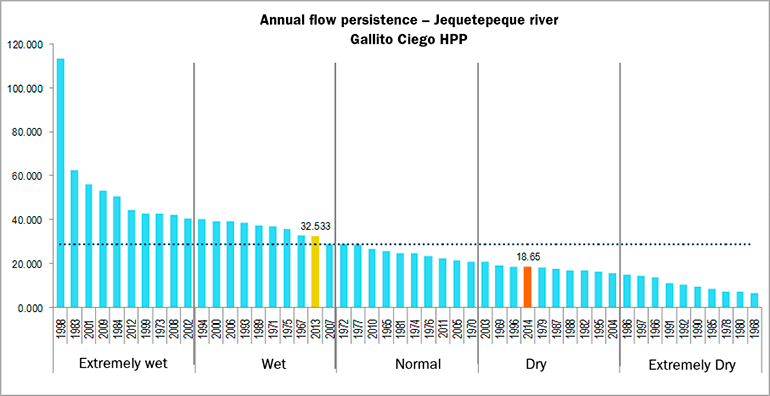

- Jequetepeque (Gallito Ciego hydropower plant): dry, with a flow of 18.65 m3/s, much lower than that in 2013 (32.53 m3/s).

The classification of each basin is shown in Charts 5 to 8.

Chart 5

Chart 6

Chart 7

Chart 8